")

India’s personal tax compliance framework is undergoing a decisive transformation, driven by digitisation, pre-filled data integration, and the introduction of simplified tax regimes by the Indian Income tax department.The Income tax return (ITR) forms for FY 2025–26 (AY 2026–27) underscore this evolution, signalling a shift from basic disclosures to more rigorous requirements for accurate, consistent, and comprehensive reporting by taxpayers, which helps authorities navigate fast processing of tax return as cross verification of claims between individual ITR vis-à-vis reporting from businesses become easier.With another tax return filing season round the corner, it is pertinent for taxpayers to plan. The first question that arises is which ITR form to choose from the various forms notified by the tax department. The selection of the appropriate ITR form depends on an individual’s specific circumstances, including residential status, nature of income, taxable income thresholds, etc.Against this backdrop, a nuanced understanding of the various ITR forms for FY 2025–26 is essential for globally mobile professionals, domestic salaried taxpayers, and individual investors to understand the basis of applicability of the different ITR forms. Please refer to the table below.

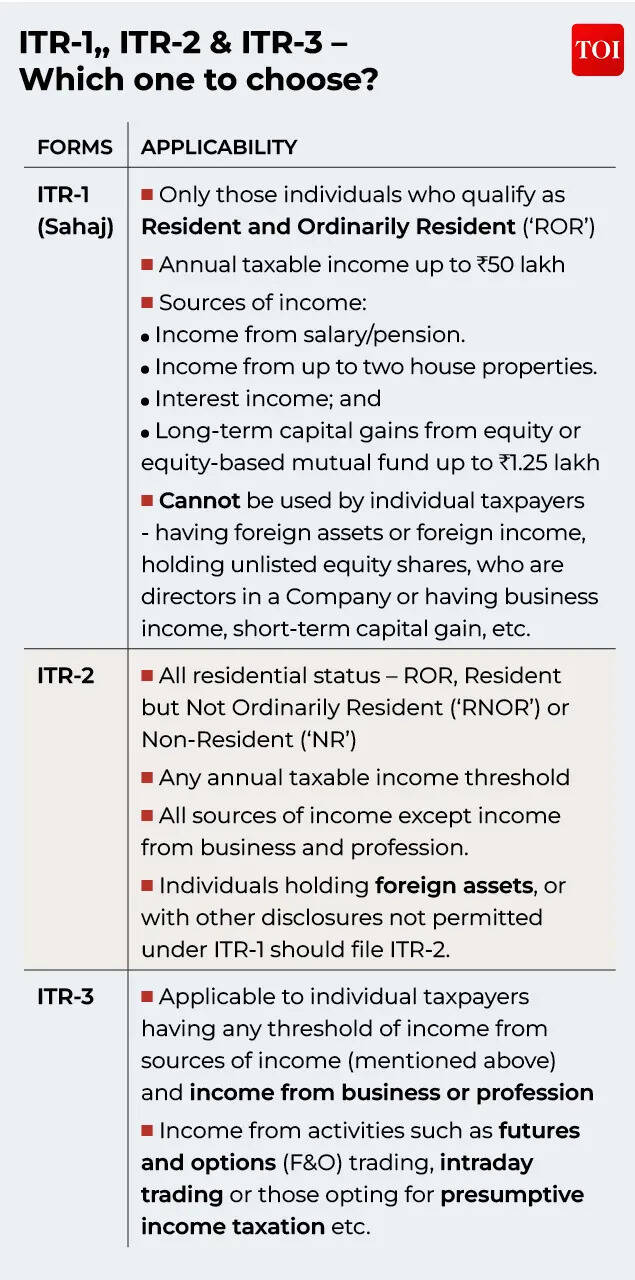

ITR-1, ITR-2 & ITR-3 – Which one to choose?

Please refer to the table for selection criteria to choose appropriate ITR forms:

ITR filing under an incorrect form may be considered defective, potentially leading to delays in processing and follow-up actions from the tax department. This remains a common error in practice. For instance, salaried taxpayers who also engage in F&O trading activities often mistakenly file ITR-2, despite being required to file ITR-3 due to the presence of business income. Such misclassification may complicate compliance and necessitate revision of the ITR.Given the increasing complexity of income profiles, individual taxpayers should carefully assess the nature and sources of their income before selecting the applicable ITR form to avoid procedural setbacks.

Residential status – Does it impact ITR form selection?

Individual taxpayers who qualify as RNOR or NR are not eligible to file ITR-1, regardless of their sources of income. In such scenarios, taxpayers are typically required to file ITR-2.Non-Resident taxation is limited to income received in India, deemed to be received in India, or income that accrues or arises in India. However, with the increasing prevalence of remote work and cross-border employment arrangements, determining the source and taxability of income has become significantly complex.Additionally, NR taxpayers are required to furnish enhanced disclosures in their ITR, including details such as their country of residence, Tax Identification Number (TIN), period of stay in India etc. Therefore, accurately determining residential status at the outset is essential to ensure correct reporting and appropriate ITR form selection.

Old vs New Personal Tax Regime – Can I revisit my tax regime in ITR?

Salaried taxpayers effectively have two opportunities to evaluate their choice of personal tax regime. First, at the start of the year when communicating preferences to the employer for withholding purposes, and again after the close of the year at the time of filing the ITR.The ITR forms require taxpayers to explicitly confirm their selected regime at the time of filing. The NPTR continues to apply by default, while opting for the old personal tax regime (‘OPTR’) requires an active selection. Notably, for salaried individuals, the choice made at the time of filing may differ from the option declared to the employer during the year.Given that the selected regime directly impacts on the availability of deductions and exemptions, taxpayers should undertake a careful reassessment before finalising their ITR.In cases where the OPTR is chosen, it is essential to ensure that all deductions and exemptions are accurately reported and supported by appropriate documentation, particularly considering increased system-driven validations and data cross-verification by the tax department based on reporting from corresponding businesses and information gathered by other sources.

ITR schedules – How to navigate reporting?

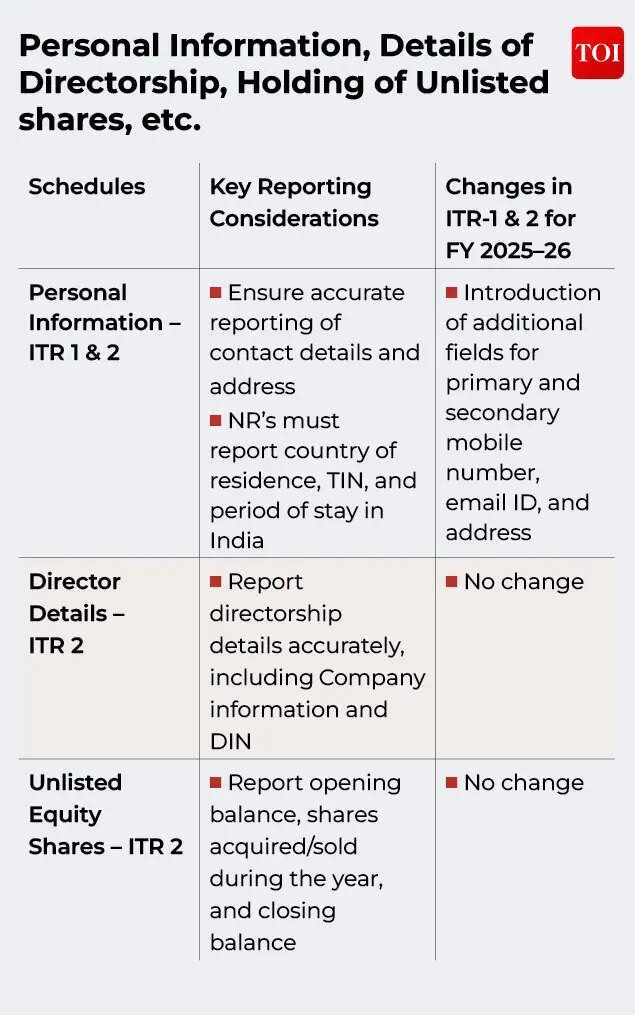

Having understood the criteria for selecting the ITR, now let us dive deeper into the forms and analyse the schedule wise reporting requirements. This serves the purpose to collate the key information and documents that individual taxpayers may require while filing the ITR forms. We have tried to break down the illustrative list below depending on the topic of reporting required in the schedules for the ease of reading and comprehension. However, consulting an expert on the subject matter is recommended before filing your tax return.Personal Information, Details of Directorship, Holding of Unlisted shares, etc.The initial section of the ITR form focuses on core taxpayer information and applicability-linked disclosures that form the foundation of filing. Accurate reporting of personal details, directorship positions, and unlisted equity shareholdings is critical, as these disclosures are increasingly used for system-driven validations by the tax department.

Reporting of Sources of Income under various headsWith increased integration of AIS, TIS, TDS disclosures, and system-driven validations, taxpayers should ensure that income is correctly classified, reconciled, and disclosed under the appropriate schedules.

Brought Forward, Carry Forward of Losses, Reporting of Exempt Income, Deductions, etc.This requires careful attention, particularly as the ITR utility now performs enhanced inter-schedule validations and cross-checks with pre-filled information. Inaccurate claims, incorrect set-offs, or incomplete disclosures may lead to denial of benefits, validation errors, or processing delays.

Foreign Tax Relief, Reporting of Foreign Income and Foreign Assets, Balances of Assets & LiabilitiesComprehensive information exchange relating to overseas income and assets between governments requires special attention of eligible taxpayers when reporting under these schedules. These schedules require detailed disclosures, consistency across multiple reporting sections, and alignment with supporting documentation to minimise scrutiny exposure for resident taxpayers with overseas income, foreign tax credits, or offshore financial interests.

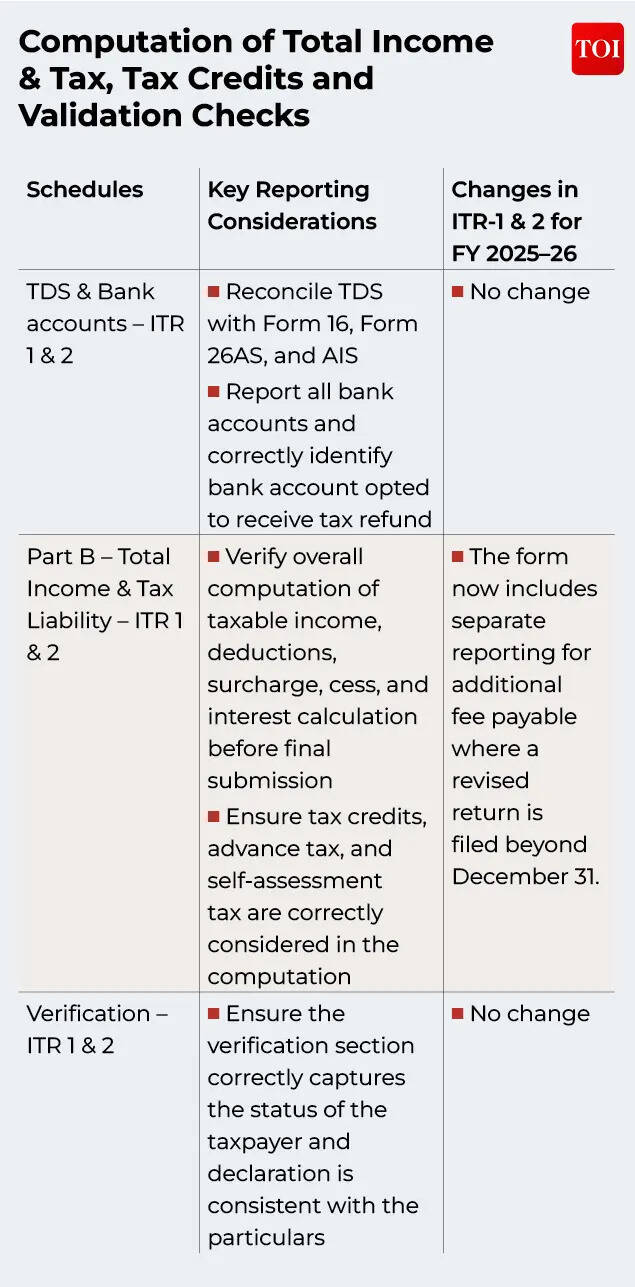

Computation of Total Income & Tax, Tax Credits and Validation ChecksThe concluding sections of the ITR form focus on computation of income from all heads, corresponding tax thereon, reconciliation of tax credits, and validation of data. Taxpayers should carefully review these to ensure consistency with Form 26AS, AIS, TIS and supporting records before electronic submission of the ITR.

Before proceeding with filing, taxpayers should ensure that the ITR form is free from validation errors. Any inconsistencies, incomplete disclosures, or incorrect entries in the ITR may trigger validation errors in the utility, which must be resolved prior to electronic submission.Act before the statutory window closes: accuracy, preparedness, and accountabilityIn an increasingly digitised tax landscape, filing an ITR can no longer be treated as a routine, year-end exercise based solely on Form 16 or tax deducted at source. Taxpayers should note that detailed instructions for completing the notified ITR forms are still awaited and may provide further guidance on certain reporting requirements.With the above context, salaried taxpayers should initiate their preparation well ahead of the filing deadline by collating supporting documentation, reconciling pre-filled information such as AIS and TIS, and carefully reviewing schedule-wise disclosures to ensure accuracy and completeness.For most individual taxpayers the due date continues to be 31 July following the end of the year except for individuals having business or professional income. Delays can trigger late filing fees, interest liabilities, restrictions on the carry forward of certain losses, and slower processing of refunds.Ultimately, in a system increasingly driven by data matching, automation, and analytics, salaried taxpayers who treat return filing as a structured and proactive compliance exercise rather than a last-minute obligation will be far better positioned to avoid discrepancies, minimize risk, and ensure a smooth and efficient filing experience.(The author, Ravi Jain, is Tax Partner at Vialto Partners. Vikas Narang, Director and Pawan Digga, Manager at Vialto Partners have also contributed to the article. Views are personal)