FM Sitharaman has stressed the need to closely monitor the three critical areas of fuel, fertiliser, and foreign exchange. (AI image)

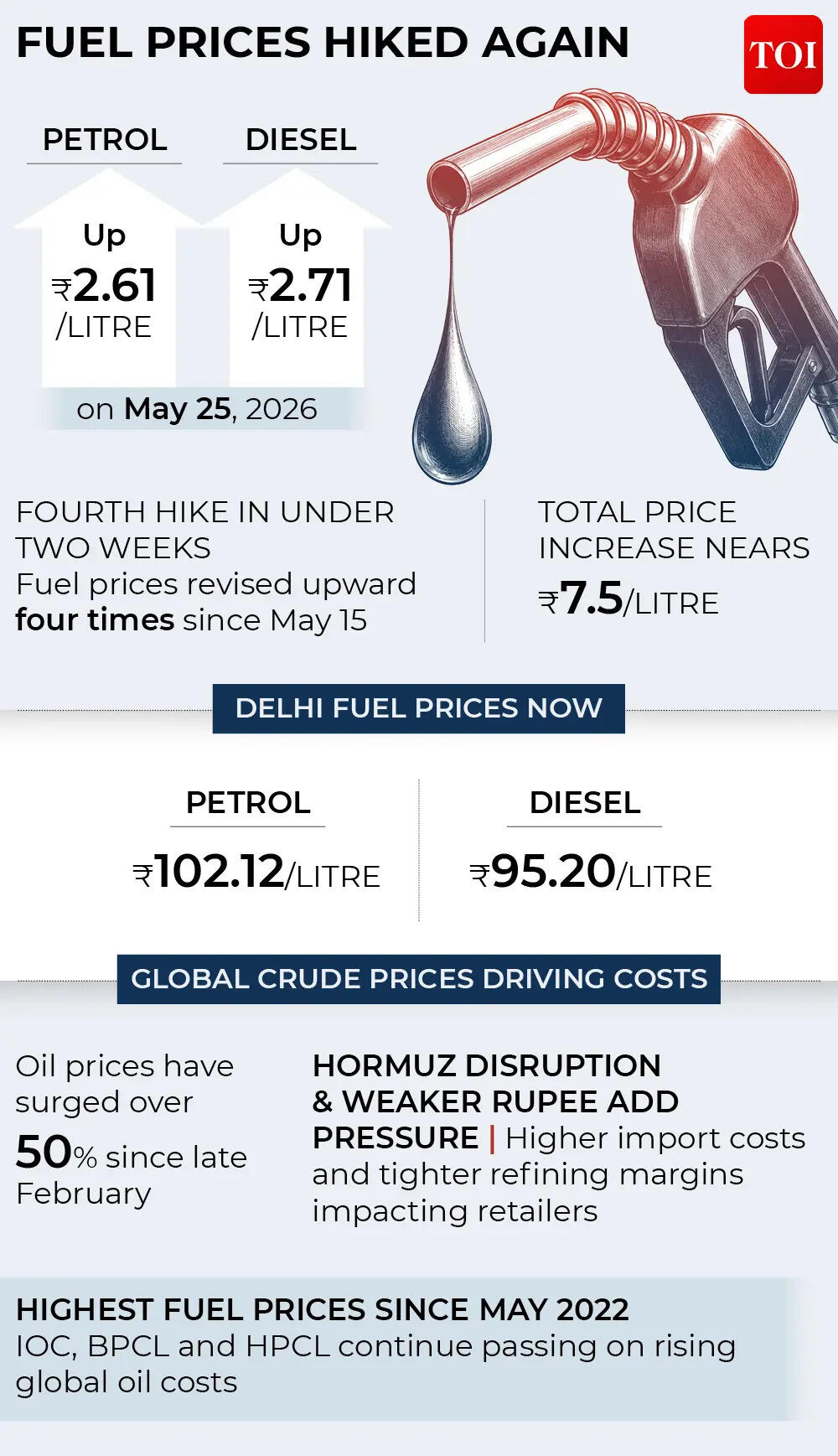

A prolonged US-Iran conflict has finally begun to hit India home, with economists signalling that the longer the crisis continues, the more difficult the situation would become for the economy. Finance Minister Nirmala Sitharaman on Monday stressed the need to closely monitor the three critical areas of fuel, fertiliser, and foreign exchange amid the ongoing West Asia conflict, while asserting that the Indian economy continues to remain resilient.Addressing an event marking the 37th foundation anniversary of Small Industries Development Bank of India (SIDBI), Sitharaman said the government’s policy response has been carefully calibrated to protect domestic economic growth. She added that the recent reduction in excise duties on petrol and diesel would have a revenue impact of nearly Rs 1 lakh crore.Sitharaman also pointed out that apart from higher crude oil prices, fertiliser prices have reached “unimaginable” levels, while elevated gold prices are creating challenges on the external sector front.Referring to the need to focus on fuel, fertiliser, and forex, she said Prime Minister Modi’s appeals should be viewed in that context. So why are the ‘3Fs’ so important? We take a look:FuelIndia’s crude oil, LPG and LNG imports are high and with energy prices rising globally, the cost is finally being passed on to consumers. Whether the government takes a revenue hit due to excise duty cuts, or consumers pay higher petrol prices, the government’s fiscal estimates take a hit. Higher crude prices feed into inflation, hitting growth. Lower revenue collections directly impact the government’s financial comfort.Petrol prices were increased by Rs 2.61 per litre and diesel by Rs 2.71 on Monday, marking the fourth hike in less than two weeks as fuel retailers continued a delayed pass-through of sharply rising global crude oil prices triggered by the Iran conflict.

With the latest revision, total fuel price increases since May 15 have reached nearly Rs 7.5 per litre.Fuel prices have now climbed to their highest levels since May 2022 after remaining largely unchanged for over two years, except for a Rs 2-per-litre reduction announced in March 2024 ahead of the national elections.Global crude prices had surged more than 50% since late February following US-Israeli strikes on Iran and disruptions to shipping activity through the Strait of Hormuz, one of the world’s most critical oil transit routes.State-run oil retailers had refrained from immediately passing on higher input costs for several weeks, with the government maintaining that the move was intended to protect consumers from inflationary pressure.Since the beginning of the conflict, domestic LPG cylinder prices have been increased by Rs 60 per 14.2-kg cylinder, while compressed natural gas (CNG) prices have risen by Rs 4 per kg since mid-May.The repeated fuel price increases are expected to intensify inflationary pressure and raise transportation and logistics costs across the economy.India’s retail inflation rose to 3.48% in April from 3.40% in March, while wholesale inflation climbed to a 42-month high of 8.3%, largely driven by higher fuel and energy prices.Last week, Prime Minister Narendra Modi urged citizens and government departments to conserve fuel, promote remote working, and reduce non-essential travel as high energy prices continued to pressure foreign exchange reserves and risk widening the current account deficit.Also Read | Timeline of petrol, diesel price hike: How rates have risen by Rs 7.5 litre in just 11 days – which cities have highest prices?FertilisersImportant for the agriculture sector, especially ahead of the monsoon season, soaring fertiliser prices are a matter of concern for the government’s fisc, especially as the prices are heavily subsidized for farmers. India imports a substantial portion of its fertiliser needs, and soaring international prices have made the government math strained.In fact, India’s fertiliser subsidy burden for FY27 could rise sharply to nearly Rs 2.4 lakh crore, an increase of around Rs 70,000 crore over current estimates, due to rising import costs of urea and other fertilisers amid the continuing West Asia conflict, government officials said last week.They also said that adequate stocks are available and imports have already been arranged to meet Kharif season demand.Aparna S Sharma, speaking on the sidelines of an inter-ministerial briefing on developments in West Asia, said the subsidy bill is expected to increase, although the exact percentage cannot yet be quantified.When asked whether the rise could be around Rs 70,000 crore, she responded that it “may be.” The Union Budget had estimated fertiliser subsidies for 2026-27 at Rs 1.7 lakh crore.Sharma said that despite disruptions in the global fertiliser supply chain because of the conflict, availability for the upcoming Kharif season remains comfortable. Current stocks stand at nearly 201 lakh tonnes, which is about 51% of the total estimated requirement of 390 lakh tonnes.She added that domestic fertiliser production is continuing at roughly 80,000 tonnes per day. Since the crisis began, output has reached around 86.2 lakh tonnes from March till now, compared with 93 lakh tonnes during the corresponding period last year.But more than the availability, it is the fiscal strain that the fertiliser subsidy bill will put on the government’s finances that is the cause of concern.ForexForeign exchange reserves are the frontline buffer for an economy, protecting it from external sector shocks. India’s forex reserves have been resilient for some time now, but with the rupee depreciating to levels of almost 97 versus the US dollar, the RBI has been forced to step in, straining forex reserves.India’s foreign exchange reserves declined by $8.094 billion to $688.894 billion during the week ending May 15, according to data released by the Reserve Bank of India on Friday.

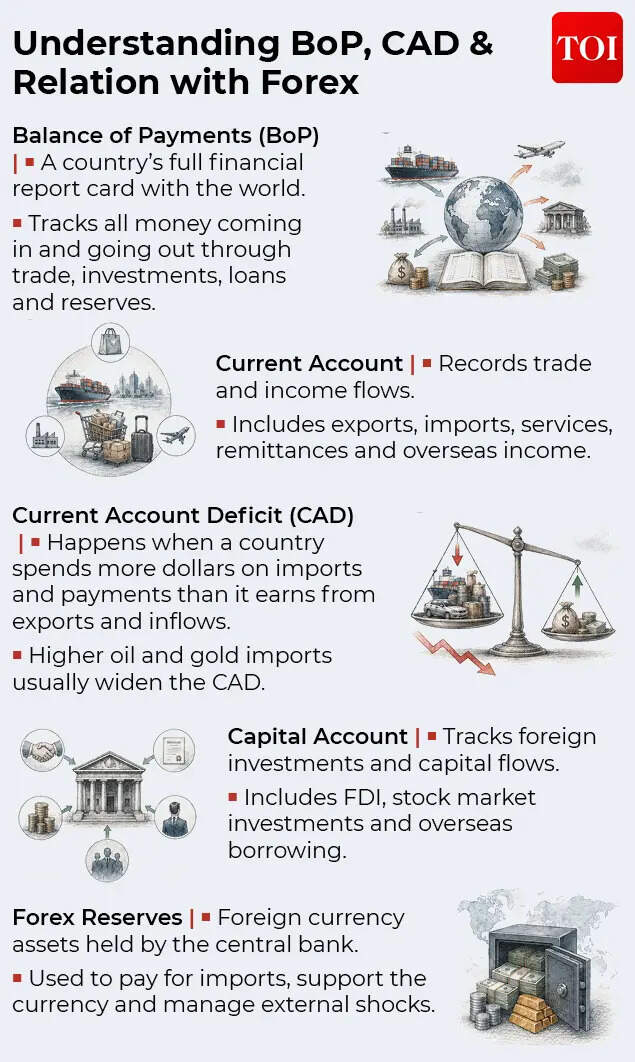

In the previous week ended May 8, the country’s forex reserves had increased by $6.295 billion to reach $696.988 billion.India’s reserves had touched a record high of $728.494 billion during the week ended February 27 this year. However, following the outbreak of the Middle East conflict, reserves witnessed several weeks of decline as pressure on the rupee prompted the RBI to intervene in the foreign exchange market through dollar sales.Prime Minister Narendra Modi has also made multiple public appeals since May 11 urging citizens to help conserve foreign exchange reserves by reducing overseas travel, cutting fuel consumption, and avoiding gold purchases for a year.Economists say India continues to hold one of the world’s largest foreign exchange reserve stockpiles, and the reserves remain strong enough to support the rupee during the ongoing phase of depreciation caused by the Middle East conflict and persistent foreign capital outflows.They believe the country’s reserve position is still sufficiently robust to absorb the oil price shock triggered by the Iran conflict, with India’s external buffers remaining considerably healthier than the levels seen during the 2013 taper tantrum.But even though India continues to maintain one of the largest forex reserve holdings globally, investors have started paying greater attention to reserve adequacy as the rupee repeatedly touches fresh record lows.A Bloomberg report based on economists’ estimates said the RBI could potentially deploy close to $150 billion from its approximately $690 billion forex reserves before India’s import cover falls to levels last witnessed during the 2013 taper tantrum, when the US Federal Reserve’s decision to scale back bond purchases triggered massive capital outflows from emerging markets.